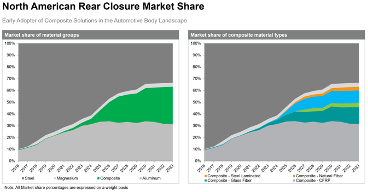

Within bodies, rear closures are quickly moving toward GFRP composites for not only weight savings, but also the secondary benefits at the assembly plant level. (See Figure 2.) The aforementioned change in mentality toward a more complete evaluation means that solutions trading one metric for another without a secondary benefit are less likely to pass rigorous examination of any large engineering firm with an established background. Otherwise, as one engineering mentor stated at General Motors, “Good engineers trade performance with an ‘or’ statement. Great engineers look for an opportunity to create ‘and’ statements in designs.” Examples of “and” statements include providing value and customer benefits, losing weight and costing less overall, and reducing ergonomic strain of plant workers and improving component packaging.

Growth areas, such as rear closures and battery enclosures, appear as easy opportunities for near-term manufacturing, but the power of composites goes well beyond this short-term sprint. Innovations in reinforcement fiber types, cross-linking resins, pultrusion and higher levels of electrical insulation are great examples of mid-term rule-breaking technologies that stand to challenge the status quo of the mechanical and electrical devices currently being produced for high-volume passenger vehicles. The history of the ceramics industry during the manufacturing adoption of spark plugs is one of the historical parallels that might be used to describe the opportunities in front of the composites industry today.

Composites have the power to use waste carbon fiber from aerospace manufacturing and to adopt higher temperature resistances than most aluminum alloys. Depending on resin choice and fiber reinforcement, composites may be the only material that can outperform the net zero-emissions goals by sequestering carbon emissions to become the only certifiably carbon negative substrate for component construction.

All of this is stated without imparting the enormous passenger safety responsibility of OEMs chasing higher electrical motor voltages. The technical capability ingredients of material performance are present in many corners of the composites market, but the true challenge lies ahead: Build the components in repeatable processes at high volume in simple ways that dovetail with engineering, maintenance and assembly ideologies.

Edwin Pope is principal research analyst in the Supply Chain & Technology Group at S&P Global Mobility. Email comments to edwin.pope@spglobal.com.

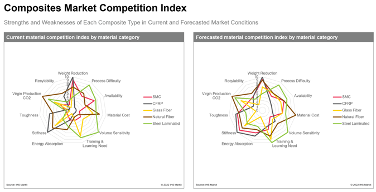

Figure 1: Composites Market Competition Index

Credit: S&P Global Mobility

Figure 2: North American Rear Closure Market Share

Credit: S&P Global Mobility